"This operational profile serves as foundational field intelligence within our broader macroeconomic tracking network. To evaluate how these localized market variables, infrastructure pipelines, and regional trade dynamics integrate into a continent-wide roadmap for capital deployment, access our master thesis directly through our core document: The Architecture of Momentum Framework."

For decades, discussions surrounding economic transformation within the Economic Community of West African States (ECOWAS) have been bottlenecked by a singular, systemic vulnerability: baseline power.

While individual member states have aggressively pursued independent national electrification strategies, fragmented grids remain structurally incapable of anchoring heavy manufacturing, automated agro-processing, or high-velocity tech infrastructure. The next phase of West African economic development cannot rely on isolated national power plants running on imported liquid fuels. Industrial scaling requires a total shift in focus from local retail utilities to a unified, regional productive-use infrastructure stack.

The future competitiveness of the region depends entirely on the operational maturity of the West African Power Pool (WAPP). By transforming individual state networks into a synchronized regional power market, West Africa can transition from localized generation deficits to a macro-grid capable of pooling diversified generation assets. However, executing this vision requires moving past a single-country export model toward a multi-anchor regional architecture.

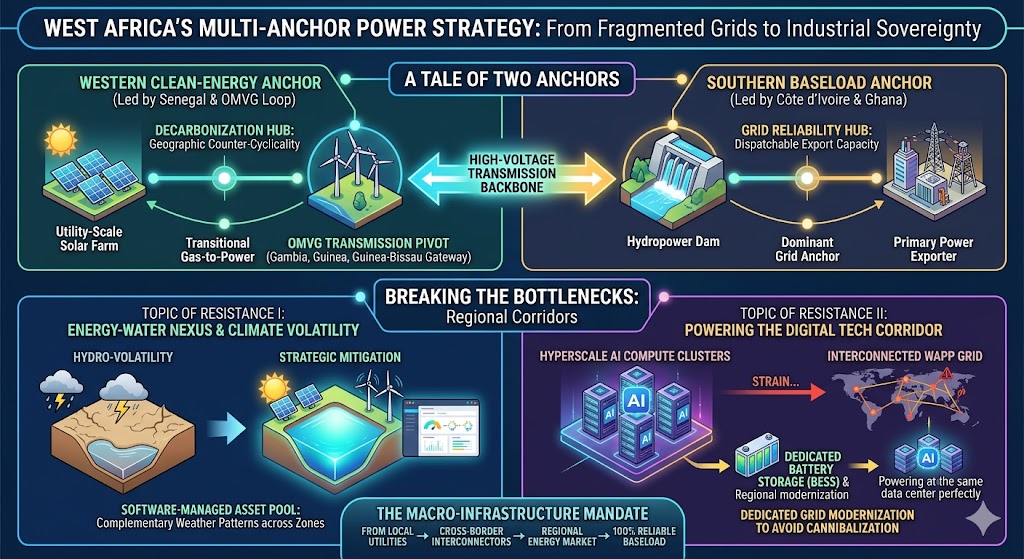

The Strategic Architecture: A Tale of Two Anchors

An integrated energy marketplace requires a sophisticated balance of geographic and asset complementarity. Rather than relying on a centralized system, the modern WAPP framework utilizes distinct sub-regions as specialized structural anchors based on their natural advantages.

1. The Southern Baseload Anchor: Côte d’Ivoire & Ghana

Historically, the southern coastal corridor has functioned as the bedrock of WAPP’s electricity architecture. Côte d’Ivoire operates as the dominant grid anchor and primary power exporter across the network, boasting an installed generation capacity that reached 2,907 MW. Backed by a modernized thermal fleet fed by domestic fields and legacy hydropower, Côte d’Ivoire exports approximately 977 GWh annually via WAPP interconnections to nations like Burkina Faso, Mali, Liberia, and Sierra Leone. Alongside Ghana, which is targeting its own 3,000 MW expansion by 2030, this southern cluster provides the vital grid stabilization and dispatchable baseline power necessary to maintain frequency across interconnected lines.

2. The Western Clean-Energy Anchor: Senegal’s Strategic Pivot

While the south provides the traditional baseline, Senegal is rapidly emerging as WAPP’s Western Decarbonization and Interconnection Anchor. Driven by aggressive capital deployment into its renewable energy sector, Senegal has built a diversified energy mix that serves as a template for regional grid balancing:

- Utility-Scale Renewables: Capitalizing on immense solar irradiation and anchoring major wind assets (such as the Taïba N’Diaye wind farm), Senegal provides the high-volume clean energy needed to green the regional grid.

- The Near-Term Gas-to-Power Trajectory: While mega-projects like the Greater Tortue Ahmeyim (GTA) LNG development are focused primarily on international export in their initial phase, Senegal has established a clear long-term domestic blueprint. The strategic, phased trajectory to transition domestic heavy fuel oil plants to natural gas will eventually provide a fast-ramping, lower-emission transitional power buffer to backstop intermittent renewables.

- The OMVG Interconnection Hub: Geographically, Senegal acts as the western gateway. Through the OMVG transmission loop, it anchors the physical flow of power between coastal neighbors (The Gambia, Guinea, Guinea-Bissau) and ties them securely into the broader regional marketplace, already helping bring localized utilities back to financial profitability.

The Elephant in the Grid: The Nigeria Paradox

A sophisticated analysis of West African power cannot ignore its largest market. Nigeria possesses the largest installed generation capacity in West Africa by far—standing at over 13,600 MW. Yet, despite this massive footprint, Nigeria’s integration into the broader WAPP macro-grid remains severely limited.

The country’s domestic power sector is crippled by severe operational constraints, achieving an average plant availability factor of just 31% due to systemic grid instability and chronic gas supply crises affecting its thermal fleet. Until Nigeria stabilizes its domestic transmission infrastructure and resolves its upstream feedstock shortages, WAPP cannot fully tap into the region’s largest potential supplier. This operational reality is precisely why the development of independent, cross-border corridors like the CLSG network and the OMVG loop among smaller coastal states is so critical—they build regional resilience around Nigeria’s structural absence.

Breaking the Bottlenecks: Critical Regional Transmission Corridors

Bandwidth needs fiber; electricity needs high-voltage transmission lines. The foundational layer of the West African energy corridor relies on heavy capital deployment into cross-border interconnectors that break down national grid isolation.

The regional infrastructure strategy is driven by major physical corridors:

Critical transnational projects—such as the CLSG network (interconnecting Côte d’Ivoire, Liberia, Sierra Leone, and Guinea) and the OMVG loop—are fundamentally rewriting the rules of regional capital allocation. These lines allow states with generation surpluses to monetize excess capacity, while allowing energy-deficient industrial zones to tap into affordable power pools.

ERERA and the Path to a Day-Ahead Market

This physical architecture is being paired with aggressive institutional reform led by the ECOWAS Regional Electricity Regulatory Authority (ERERA). Far from a passive administrative body, ERERA has laid the groundwork for a formalized Day-Ahead Market (DAM) for power.

Regulators successfully validated regional DAM tariffs and oversaw the first massive synchronization trial with uninterrupted power flows across twelve West African nations. By standardizing regional grid codes, transmission pricing, and cross-border contracts, ERERA is actively transforming electricity from a rigid state utility into a highly liquid, traded regional commodity. This reduces utility cost structures and guarantees long-term pricing visibility for heavy industry.

Topic of Resistance I: The Energy-Water Nexus and Climate Volatility

As West Africa seeks to diversify its regional energy mix, the primary structural resistance point threatening long-term grid stability is the energy-water nexus.

Historically, large-scale hydropower has served as a core baseload asset for West African power architecture. However, heavy reliance on major river basins introduces extreme vulnerability to climate-driven hydrological fluctuations and seasonal droughts. When water volumes drop, regional generation capacity collapses, forcing utilities back onto expensive emergency fossil-fuel generation.

To mitigate this systemic vulnerability, the region’s multi-anchor framework utilizes geographic counter-cyclicality. By treating weather patterns across separate geographic zones as complementary inputs, the WAPP can deploy Senegal’s coastal solar and wind assets to buffer inland hydropower strains during low-rainfall periods, managing regional resources as a single, diversified asset pool.

Topic of Resistance II: Powering the Digital Tech Corridor

The regional energy framework is the absolute prerequisite layer for the expanding digital economy. The single greatest threat to West Africa’s digital sovereignty is the massive, uninterrupted power draw required by modern AI Data Centers and enterprise cloud infrastructure.

Hyperscale computing clusters are essentially machines that transform continuous electricity into digital processing power. Unlike light manufacturing or residential consumption, an AI data center cannot tolerate micro-fluctuations in voltage, nor can it operate on intermittent power profiles.

To resolve this future resistance point, regional infrastructure financing must explicitly couple data center deployment with dedicated, localized grid modernization. Compute corridors must be built alongside utility-scale clean energy zones equipped with massive utility-scale battery energy storage systems (BESS). Without direct coordination between the WAPP, grid anchors like Côte d’Ivoire, and clean energy leaders like Senegal, the processing demands of artificial intelligence risk cannibalizing the energy capacity needed for industrial manufacturing.

The Macro-Infrastructure Mandate

Energy integration across West Africa is no longer an issue of extending domestic utility lines; it is a macro-regional industrial mandate. The ultimate success of the African Continental Free Trade Area (AfCFTA) within West Africa will not be determined by trade policies, but by the physical capacity of the synchronized grid to power the factories, logistics hubs, and compute architectures that process value-added goods.

For institutional investors, development finance institutions (DFIs), and infrastructure funds, the investment thesis must shift away from localized, single-country generation assets. The true source of long-term economic value creation lies in financing the cross-border interconnectors, regional energy storage systems, and market-clearing mechanisms that turn the entire ECOWAS sub-region into a singular, high-velocity power pool.

Stay Ahead of the Market Subscribe to our newsletter for the latest insights on African infrastructure and industrial policy.

Related Reading

Beyond Isolated Grids: The Multi-Anchor Strategy Powering West Africa’s Industrial Leap

The Evolving ECOWAS Regional Engine

The Big Picture: The Central Artery of the West

Building the West African Digital Tech Corridor: Regional Digital Infrastructure